# install.packages("randomizr")

## Y0 is fixed in most field experiments.

## So we only generate it once:

make_Y0 <- function(N){ rnorm(n = N) }

repeat_experiment_and_test <- function(N, Y0, tau){

Y1 <- Y0 + tau

Z <- complete_ra(N = N)

Yobs <- Z * Y1 + (1 - Z) * Y0

estimator <- lm_robust(Yobs ~ Z)

pval <- estimator$p.value[2]

return(pval)

}ECON6037 Experimental Economics

Statistical power

Gerhard Riener

February 20, 2024

What is power?

What is power?

We want to separate signal from noise.

Power = probability of rejecting null hypothesis, given true effect \(\ne 0\).

In other words, it is the ability to detect an effect given that it exists.

Formally: \((1 - \beta)\) (1- Error type) error rate.

Thus, power \(\in (0, 1)\) .

Standard thresholds: \(0.8\) or \(0.9\).

Starting point for power analysis

Power analysis is something we do before we run a study.

Helps you figure out the sample you need to detect a given effect size.

Or helps you figure out a minimal detectable difference given a set sample size.

May help you decide whether to run a study.

It is hard to learn from an under-powered null finding.

- Was there an effect, but we were unable to detect it? or was there no effect? We can’t say.

Power

Say there truly is a treatment effect and you run your experiment many times. How often will you get a statistically significant result?

Some guesswork to answer this question.

How big is your treatment effect?

How many units are treated, measured?

How much noise is there in the measurement of your outcome?

Approaches to power calculation

Analytical calculations of power

Simulation

Power calculation tools

Interactive

R Packages

DeclareDesign, see also https://declaredesign.org/

Analytical calculations of power

Analytical calculations of power

Formula: \[\begin{align*} \text{Power} &= \Phi\left(\frac{|\tau| \sqrt{N}}{2\sigma}- \Phi^{-1}(1- \frac{\alpha}{2})\right) \end{align*}\]

Components:

- \(\Phi\): standard normal CDF is monotonically increasing

- \(\tau\): the effect size

- \(N\): the sample size

- \(\sigma\): the standard deviation of the outcome

- \(\alpha\): the significance level (typically 0.05)

Example: Analytical calculations of power

Optimal Sample Size Calculation

Formula by List et al. (2011)

Actual question for experimental economists: How large should the sample be?

Applicable for experiments with a dichotomous treatment.

Outcome is continuous.

t-test used for differences between treatment and control groups.

Optimal Sample Size: Assumptions

Distribution Assumptions

Outcomes in treatments are normally distributed: \(Y_{it} |X_i \sim N(\mu_t , \sigma^2_t )\).

\(\delta\) is the minimum average treatment effect detectable.

Null hypothesis \(H_0\): \(\mu_0 = \mu_1\).

Alternative hypothesis \(H_1\): \(\mu_0 \neq \mu_1\).

Optimal Sample Size: Equal Variances

Sample Size Formula

If \(\sigma_0 = \sigma_1 = \sigma\), the optimal sample size is:

\[N_0^* = N_1^* = N^* = 2(t_{\alpha/2} + t_\beta )^2(\frac{\sigma}{\delta})^2\]

Note: Just see that this formula is an inverse of calculating p-value.

Optimal Sample Size: Example

Sample Calculation

- Significance level \(\alpha\): 0.05.

- Power \(1-\beta\): 0.80.

- From standard normal tables: \(t_{\alpha/2} = 1.96\), \(t_\beta = 0.84\).

- To detect a half standard deviation change, you need 64 observations per treatment group. \[N^*= 2(1.96 + 0.84)^2 2^2 = 64\]

Optimal Sample Size: Key Considerations

Factors Affecting Sample Size

Increases with the variance of outcomes.

Non-linearly dependent on the significance level and power.

Decreases with the square of the minimum detectable effect.

Relative distribution of subjects across groups relates to outcome variances.

Challenges in experimental economics: unknown effect size and variance, multiple hypothesis testing, and status quo bias.

Limitations to analytical power calculations

Limitations to analytical power calculations

Only derived for some test statistics (differences of means)

Makes specific assumptions about the data-generating process

Incompatible with more complex designs

Simulation-based power calculation

Simulation-based power calculation

Create dataset and simulate research design.

Assumptions are necessary for simulation studies, but you make your own.

For the DeclareDesign approach, see https://declaredesign.org/

Steps

Define the sample and the potential outcomes function.

Define the treatment assignment procedure.

Create data.

Assign treatment, then estimate the effect.

Do this many times.

Examples

Complete randomization

With covariates

With cluster randomization

Example: Simulation-based power for complete randomization

Example: Simulation-based power for complete randomization

Example: Using DeclareDesign

P0 <- declare_population(N,u0=rnorm(N))

# declare Y(Z=1) and Y(Z=0)

O0 <- declare_potential_outcomes(Y_Z_0 = 5 + u0, Y_Z_1 = Y_Z_0 + tau)

# design is to assign m units to treatment

A0 <- declare_assignment(Z=conduct_ra(N=N, m=round(N/2)))

# estimand is the average difference between Y(Z=1) and Y(Z=0)

estimand_ate <- declare_inquiry(ATE=mean(Y_Z_1 - Y_Z_0))

R0 <- declare_reveal(Y,Z)

design0_base <- P0 + A0 + O0 + R0

## For example:

design0_N100_tau25 <- redesign(design0_base,N=100,tau=.25)

dat0_N100_tau25 <- draw_data(design0_N100_tau25)

head(dat0_N100_tau25) ID u0 Z Y_Z_0 Y_Z_1 Y

1 001 -0.2060421 0 4.793958 5.043958 4.793958

2 002 -0.5874759 0 4.412524 4.662524 4.412524

3 003 -0.2908008 1 4.709199 4.959199 4.959199

4 004 -2.5648996 0 2.435100 2.685100 2.435100

5 005 -1.8967213 0 3.103279 3.353279 3.103279

6 006 -1.6400715 1 3.359928 3.609928 3.609928[1] 0.25[1] 0.5569162Example: Using DeclareDesign

(Intercept) Z

4.8457631 0.5569162 E0 <- declare_estimator(Y~Z,model=lm_robust,label="t test 1",

inquiry="ATE")

t_test <- function(data) {

test <- with(data, t.test(x = Y[Z == 1], y = Y[Z == 0]))

data.frame(statistic = test$statistic, p.value = test$p.value)

}

T0 <- declare_test(handler=label_test(t_test),label="t test 2")

design0_plus_tests <- design0_base + E0 + T0

design0_N100_tau25_plus <- redesign(design0_plus_tests,N=100,tau=.25)

## Only repeat the random assignment, not the creation of Y0. Ignore warning

names(design0_N100_tau25_plus)[1] "P0" "A0" "O0" "R0" "t test 1" "t test 2"design0_N100_tau25_sims <- simulate_design(design0_N100_tau25_plus,

sims=c(1,100,1,1,1,1)) # only repeat the random assignment

# design0_N100_tau25_sims has 200 rows (2 tests * 100 random assignments)

# just look at the first 6 rows

head(design0_N100_tau25_sims) design N tau sim_ID estimator term estimate std.error

1 design0_N100_tau25_plus 100 0.25 1 t test 1 Z 0.1107677 0.2149666

2 design0_N100_tau25_plus 100 0.25 1 t test 2 <NA> NA NA

3 design0_N100_tau25_plus 100 0.25 2 t test 1 Z 0.2458211 0.2154258

4 design0_N100_tau25_plus 100 0.25 2 t test 2 <NA> NA NA

5 design0_N100_tau25_plus 100 0.25 3 t test 1 Z 0.5463041 0.2133367

6 design0_N100_tau25_plus 100 0.25 3 t test 2 <NA> NA NA

statistic p.value conf.low conf.high df outcome inquiry step_1_draw

1 0.5152789 0.6075185 -0.3158265 0.5373619 98 Y ATE 1

2 0.5152789 0.6075435 NA NA NA <NA> <NA> 1

3 1.1410944 0.2566114 -0.1816843 0.6733266 98 Y ATE 1

4 1.1410944 0.2566230 NA NA NA <NA> <NA> 1

5 2.5607596 0.0119701 0.1229443 0.9696640 98 Y ATE 1

6 2.5607596 0.0120273 NA NA NA <NA> <NA> 1

step_2_draw

1 1

2 1

3 2

4 2

5 3

6 3Example: Using DeclareDesign

Now count the number of simulations where the p-value is less than 0.05.

# A tibble: 2 × 2

estimator pow

<chr> <dbl>

1 t test 1 0.2

2 t test 2 0.2Power with covariate adjustment

Covariate adjustment and power

Covariate adjustment can improve power because it mops up variation in the outcome variable.

If prognostic, covariate adjustment can reduce variance dramatically. Lower variance means higher power.

If non-prognostic, power gains are minimal.

All covariates must be pre-treatment. Do not drop observations on account of missingness.

- See the module on threats to internal validity and the 10 things to know about covariate adjustment.

Freedman’s bias as n of observations decreases and K covariates increases.

Blocking

Blocking: randomly assign treatment within blocks

“Ex-ante” covariate adjustment

Higher precision/efficiency implies more power

Reduce “conditional bias”: association between treatment assignment and potential outcomes

Benefits of blocking over covariate adjustment clearest in small experiments

Example: Simulation-based power with a covariate

## Y0 is fixed in most field experiments. So we only generate it once

make_Y0_cov <- function(N){

u0 <- rnorm(n = N)

x <- rpois(n=N,lambda=2)

Y0 <- .5 * sd(u0) * x + u0

return(data.frame(Y0=Y0,x=x))

}

## X is moderarely predictive of Y0.

test_dat <- make_Y0_cov(100)

test_lm <- lm_robust(Y0~x,data=test_dat)

summary(test_lm)

Call:

lm_robust(formula = Y0 ~ x, data = test_dat)

Standard error type: HC2

Coefficients:

Estimate Std. Error t value Pr(>|t|) CI Lower CI Upper DF

(Intercept) 0.1100 0.18801 0.5852 5.598e-01 -0.2631 0.4831 98

x 0.4404 0.08137 5.4128 4.411e-07 0.2790 0.6019 98

Multiple R-squared: 0.231 , Adjusted R-squared: 0.2232

F-statistic: 29.3 on 1 and 98 DF, p-value: 4.411e-07Example: Simulation-based power with a covariate

Example: Simulation-based power with a covariate

Power for cluster randomization

Power and clustered designs

Recall the randomization module.

Given a fixed \(N\), a clustered design is weakly less powered than a non-clustered design.

- The difference is often substantial.

We have to estimate variance correctly:

- Clustering standard errors (the usual)

- Randomization inference

To increase power:

- Better to increase number of clusters than number of units per cluster.

- How much clusters reduce power depends critically on the intra-cluster correlation (the ratio of variance within clusters to total variance).

A note on clustering in observational research

Often overlooked, leading to (possibly) wildly understated uncertainty.

Frequentist inference based on ratio \(\hat{\beta}/\hat{se}\)

If we underestimate \(\hat{se}\), we are much more likely to reject \(H_0\). (Type-I error rate is too high.)

Many observational designs much less powered than we think they are.

Example: Simulation-based power for cluster randomization

## Y0 is fixed in most field experiments. So we only generate it once

make_Y0_clus <- function(n_indivs,n_clus){

# n_indivs is number of people per cluster

# n_clus is number of clusters

clus_id <- gl(n_clus,n_indivs)

N <- n_clus * n_indivs

u0 <- fabricatr::draw_normal_icc(N=N,clusters=clus_id,ICC=.1)

Y0 <- u0

return(data.frame(Y0=Y0,clus_id=clus_id))

}test_dat <- make_Y0_clus(n_indivs=10,n_clus=100)

# confirm that this produces data with 10 in each of 100 clusters

table(test_dat$clus_id)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10

21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10

41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60

10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10

61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80

10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100

10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 10 Example: Simulation-based power for cluster randomization

[1] 0.09654799Example: Simulation-based power for cluster randomization

Example: Simulation-based power for cluster randomization

Example: Simulation-based power for cluster randomization (DeclareDesign)

P1 <- declare_population(N = n_clus * n_indivs,

clusters=gl(n_clus,n_indivs),

u0=draw_normal_icc(N=N,clusters=clusters,ICC=.2))

O1 <- declare_potential_outcomes(Y_Z_0 = 5 + u0, Y_Z_1 = Y_Z_0 + tau)

A1 <- declare_assignment(Z=conduct_ra(N=N, clusters=clusters))

estimand_ate <- declare_inquiry(ATE=mean(Y_Z_1 - Y_Z_0))

R1 <- declare_reveal(Y,Z)

design1_base <- P1 + A1 + O1 + R1 + estimand_ate

## For example:

design1_test <- redesign(design1_base,n_clus=10,n_indivs=100,tau=.25)

test_d1 <- draw_data(design1_test)

# confirm all individuals in a cluster have the same treatment assignment

with(test_d1,table(Z,clusters)) clusters

Z 1 2 3 4 5 6 7 8 9 10

0 100 0 100 100 100 0 0 100 0 0

1 0 100 0 0 0 100 100 0 100 100# three estimators, differ in se_type:

E1a <- declare_estimator(Y~Z,model=lm_robust,clusters=clusters,

se_type="CR2", label="CR2 cluster t test",

inquiry="ATE")

E1b <- declare_estimator(Y~Z,model=lm_robust,clusters=clusters,

se_type="CR0", label="CR0 cluster t test",

inquiry="ATE")

E1c <- declare_estimator(Y~Z,model=lm_robust,clusters=clusters,

se_type="stata", label="stata RCSE t test",

inquiry="ATE")

design1_plus <- design1_base + E1a + E1b + E1c

design1_plus_tosim <- redesign(design1_plus,n_clus=10,n_indivs=100,tau=.25)Example: Simulation-based power for cluster randomization (DeclareDesign)

## Only repeat the random assignment, not the creation of Y0. Ignore warning

## We would want more simulations in practice.

set.seed(12355)

design1_sims <- simulate_design(design1_plus_tosim,

sims=c(1,1000,rep(1,length(design1_plus_tosim)-2)))

design1_sims %>% group_by(estimator) %>%

summarize(pow=mean(p.value < .05),

coverage = mean(estimand <= conf.high & estimand >= conf.low),

.groups="drop")# A tibble: 3 × 3

estimator pow coverage

<chr> <dbl> <dbl>

1 CR0 cluster t test 0.155 0.911

2 CR2 cluster t test 0.105 0.936

3 stata RCSE t test 0.131 0.918Example: Simulation-based power for cluster randomization (DeclareDesign)

Example: Simulation-based power for cluster randomization (DeclareDesign)

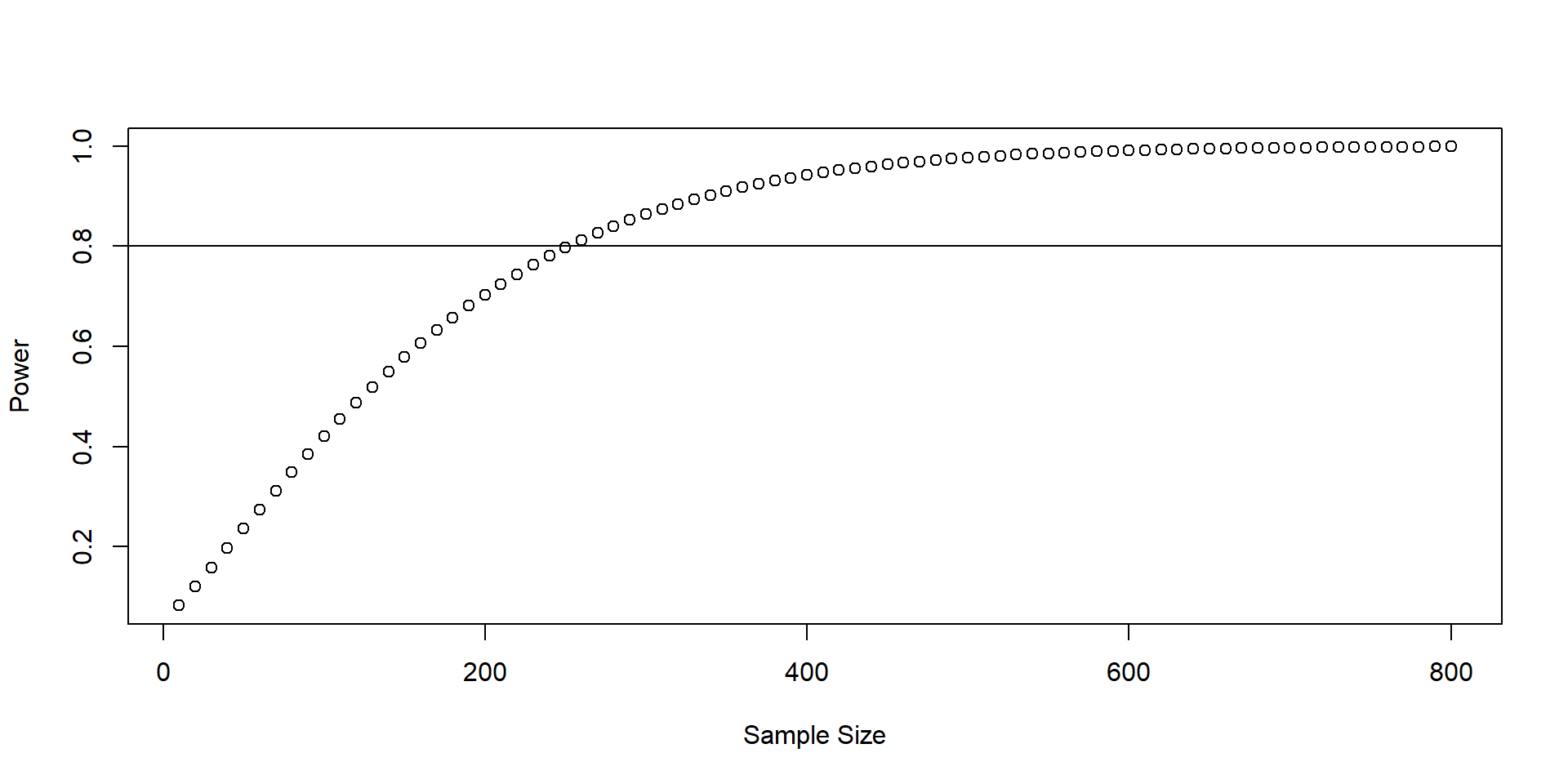

Comparative statics

Comparative Statics

- Power is:

- Increasing in \(N\)

- Increasing in \(|\tau|\)

- Decreasing in \(\sigma\)

Power by sample size

Power by treatment effect size

Conclusion: How to improve your power

- Increase the \(N\)

- If clustered, increase the number of clusters if at all possible

Strengthen the treatment

Improve precision

Covariate adjustment

Blocking

- Better measurement of the outcome variable

Comments

Know your outcome variable.

What effects can you realistically expect from your treatment?

What is the plausible range of variation of the outcome variable?